The Sears (Willis) Tower was the last of the “free market” RBSes, in the sense that it was constructed as a corporate headquarters and its height was based on the needs of the corporation. In the late 1960s, Sears, Roebuck & Co. wanted a new headquarters to centralize its staff, while also having extra space to use in the future. The bundled tube design, along with a large lot and generous zoning regulations, meant that it could get the world’s tallest building simply based on the underlying economics.

The World Trade Center’s twin towers, on the other hand, were built by a government agency when municipal and state governments were attempting “urban renewal” programs. The World Trade Center was proposed to revitalize lower Manhattan. New York State turned to the Port Authority (PA) of New York as an independent government entity that had the financial and engineering might to effectuate it. Under the auspices of PA Director Austin Tobin, the project was expanded to 13.63 million square feet (126,6270 square meters), along with a plan to produce the world’s tallest twin towers (Gillespie 1999).

Economic Analysis

The main lessons were not just on the structural side, but also regarding their economics. The Sears (Willis) Tower was built to accommodate its present and future expected demand for 3.7 million rentable square feet (343,741 square meters) of space. Additionally, Sears wanted very large floor plans on the lower floors for its phone banks and mail-order business. While they served the company at the time, the space was cavernous and had little sunlight in the interiors, which, unwittingly, dampened its future economic value.

Similarly, in the early 1970s, when opened, the Twin Towers put on the market vast quantities of rental space. Even though the buildings were meant to house international trade concerns, New York’s port-related jobs were declining. To help fill the buildings, the Port Authority turned to government agencies to pick up the slack, with New York State renting some 20 percent of the total space (Fusscas 1992). The World Trade Center contributed to an office glut in the mid-1970s (Horsely 1974).

The combined factors of the “slum clearance” process, its impact on the rental market, and government agencies filling the buildings, meant that the Twin Towers were clouded in controversy, and dampened the appetite for future American record-breakers.

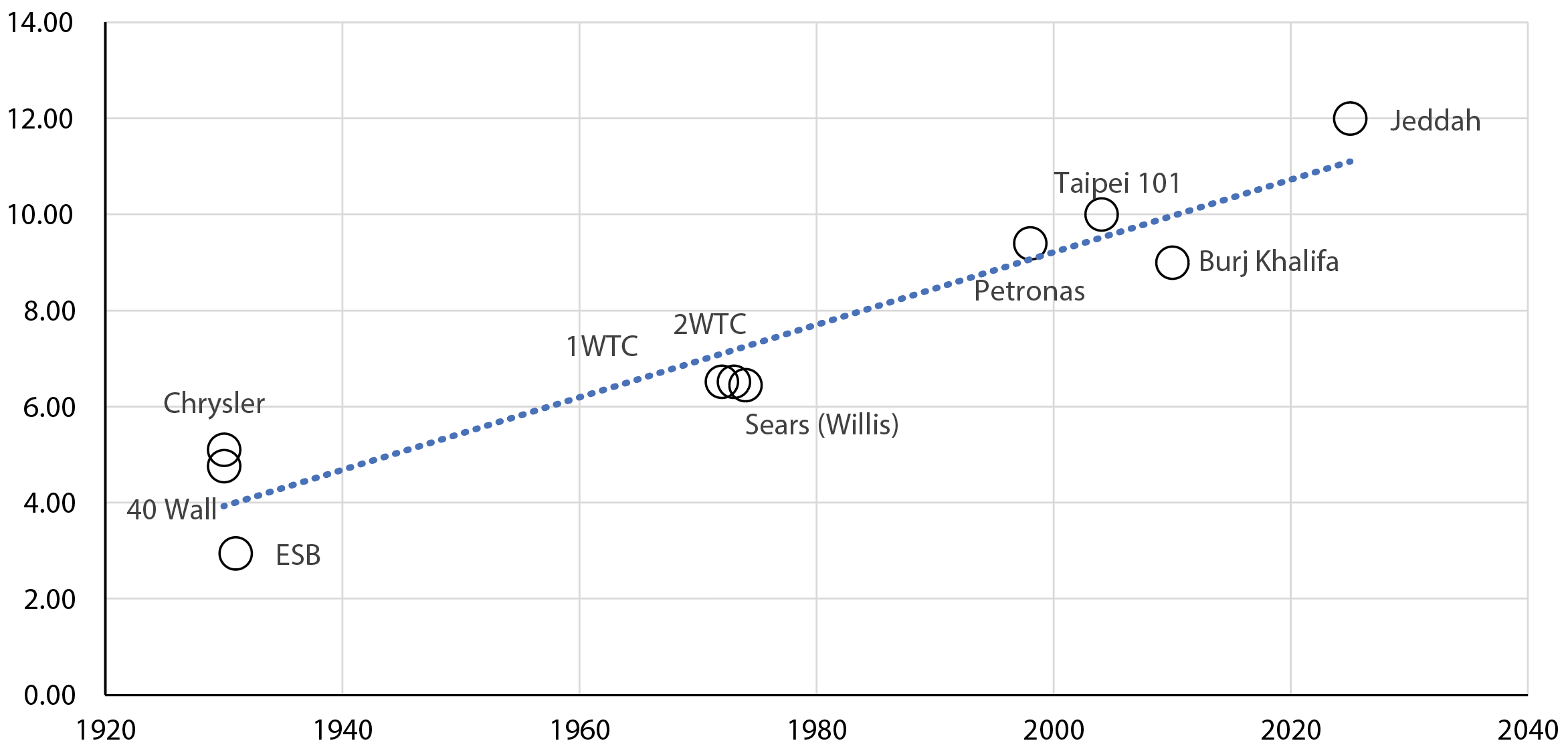

Another lesson was that if buildings were going to be taller, they would have to get thinner to keep costs manageable and to limit the “self-sabotaging” nature of mega-sized skyscrapers. The Empire State Building and Chrysler Building have aspect ratios (the height divided by the width at the base) of 3:1 and 5:1, respectively. The Sears Tower and each of the Twin Towers were about 6.5:1. The Petronas Towers (1998), the TAIPEI 101 (2004), and the Burj Khalifa (2010) are all 9:1 or higher. The Jeddah Tower, before being placed on hold, was expected to have an aspect ratio of 12:1 (see Figure 8).

However, looking back over the long run, economically speaking, the Twin Towers were a success. By 1989, the World Trade Center was earning a gross operating income of over US$110 million per year, more than one-third of the Port Authority’s total operating income. The Twin Towers also rented at a premium compared to similar buildings downtown (Fusscas 1992.)

The decline of Sears’ profitability in the 1980s, along with a general office glut in the 1990s meant that the Sears Tower was consistently under-rented. Sears defaulted on its building in 1994. In 2009, the new owners made a deal with the Willis Group, a London-based insurance broker, which purchased the naming rights and rented a large block of space.

In 2015, in a show of optimism, the Blackstone Group, a private equity firm, purchased the building for US$1.5 billion, the highest price ever paid for a Chicago skyscraper. Blackstone put in another US$670 million for an upgrade, and today the building is holding its own, even during the pandemic (Gallun 2022).